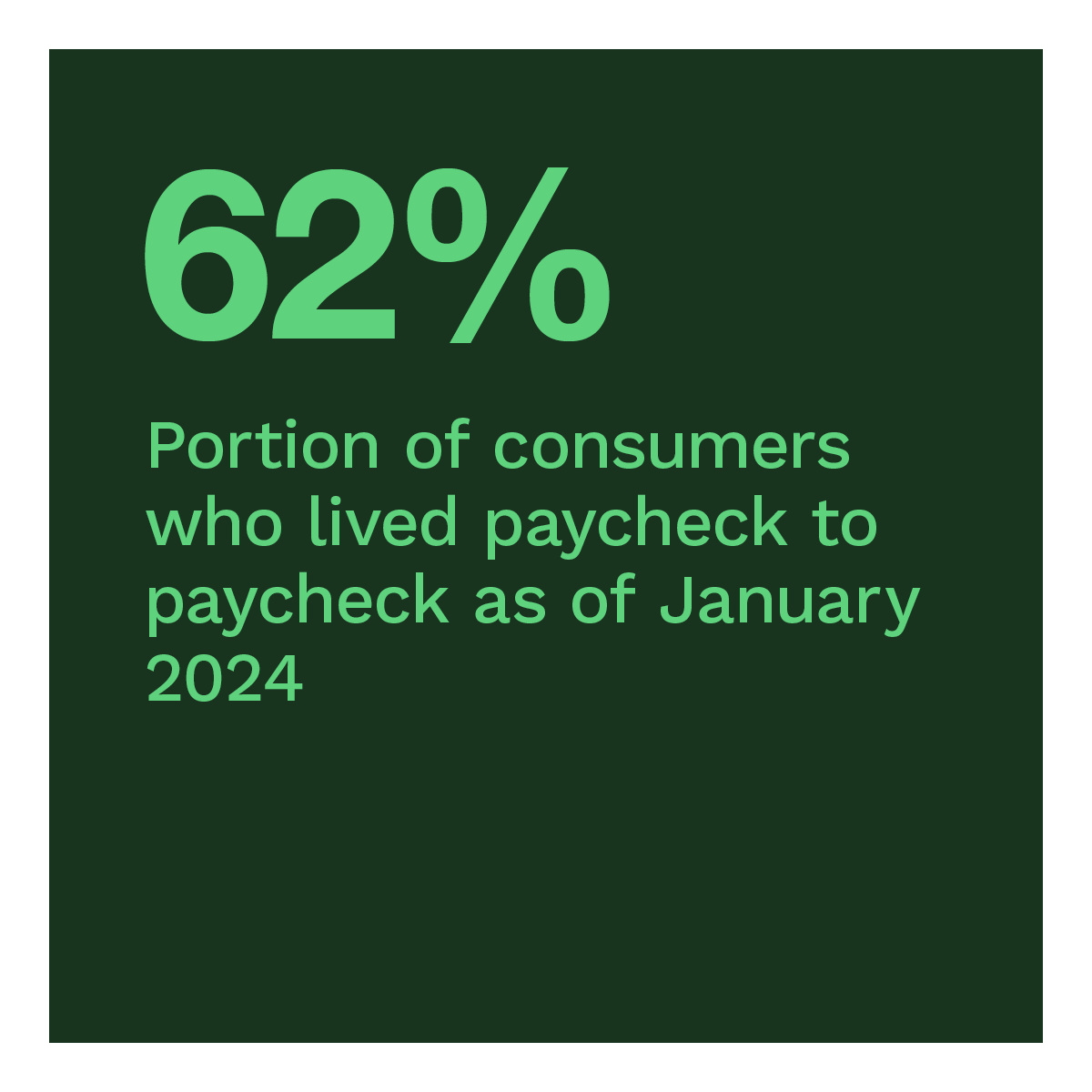

The prices of goods and services will continue to weigh on U.S. consumers’ wallets in 2024. Most consumers still say they live paycheck to paycheck. Overall, 62% of consumers lived this way as of January 2024, down from 60% last year. This increase suggests the rising cost of living may be taking its toll on consumer finances — including high-income consumers.

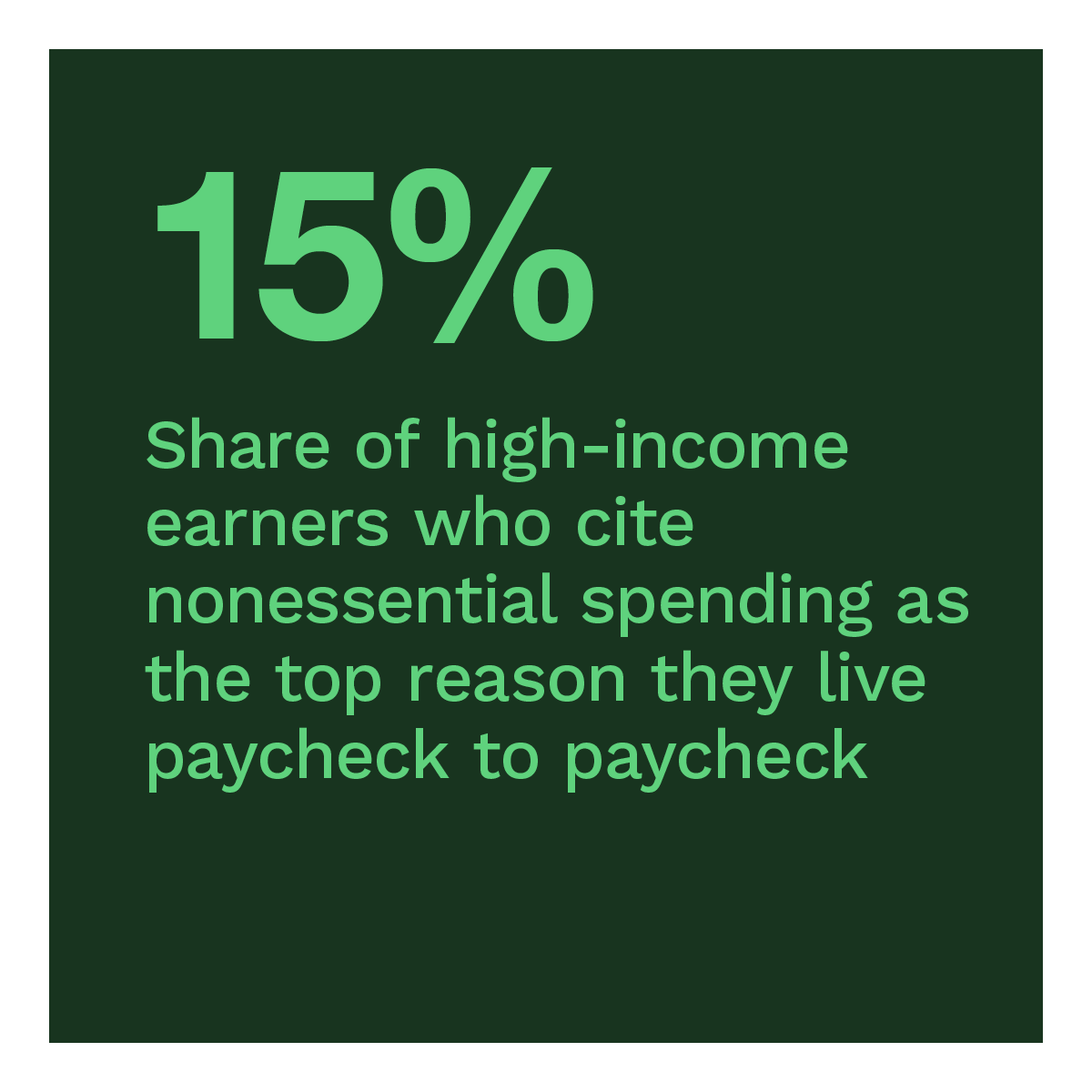

More than one-third of those annually earning more than $200,000 saying they live paycheck to paycheck. While rising housing and food costs impact high-income consumers, other factors — such as nonessential spending, paying expenses for others and drawing on savings due to unexpected expenses — may particularly inform their financial lifestyles. Wages for high earners are more likely to have kept up with inflation, possibly explaining their increase in discretionary spending. Just 18% of overall wage earners say their incomes have kept up with inflation, yet 27% of high earners say so.

These are a few of the findings detailed in this edition of “New Reality Check: The Paycheck-to-Paycheck Report,” a PYMNTS Intelligence exclusive report. This edition, “Why One-Third of High Earners Live Paycheck to Paycheck,” examines the financial lifestyles of U.S. consumers and the factors contributing to their financial status. This edition draws on insights from a survey of 4,285 U.S. consumers conducted from Jan. 9 to Jan. 16 and an analysis of other economic data.

Other key findings from the report include the following:

The increase in consumers living this financial lifestyle is evident across income brackets. The share of consumers living this financial lifestyle and annually earning more than $100,000 has increased from last January, currently standing at 48%. This share includes 36% of those annually earning more than $200,000. Even though they tend to have higher incomes, millennials are more likely to live paycheck to paycheck, as do urban consumers.

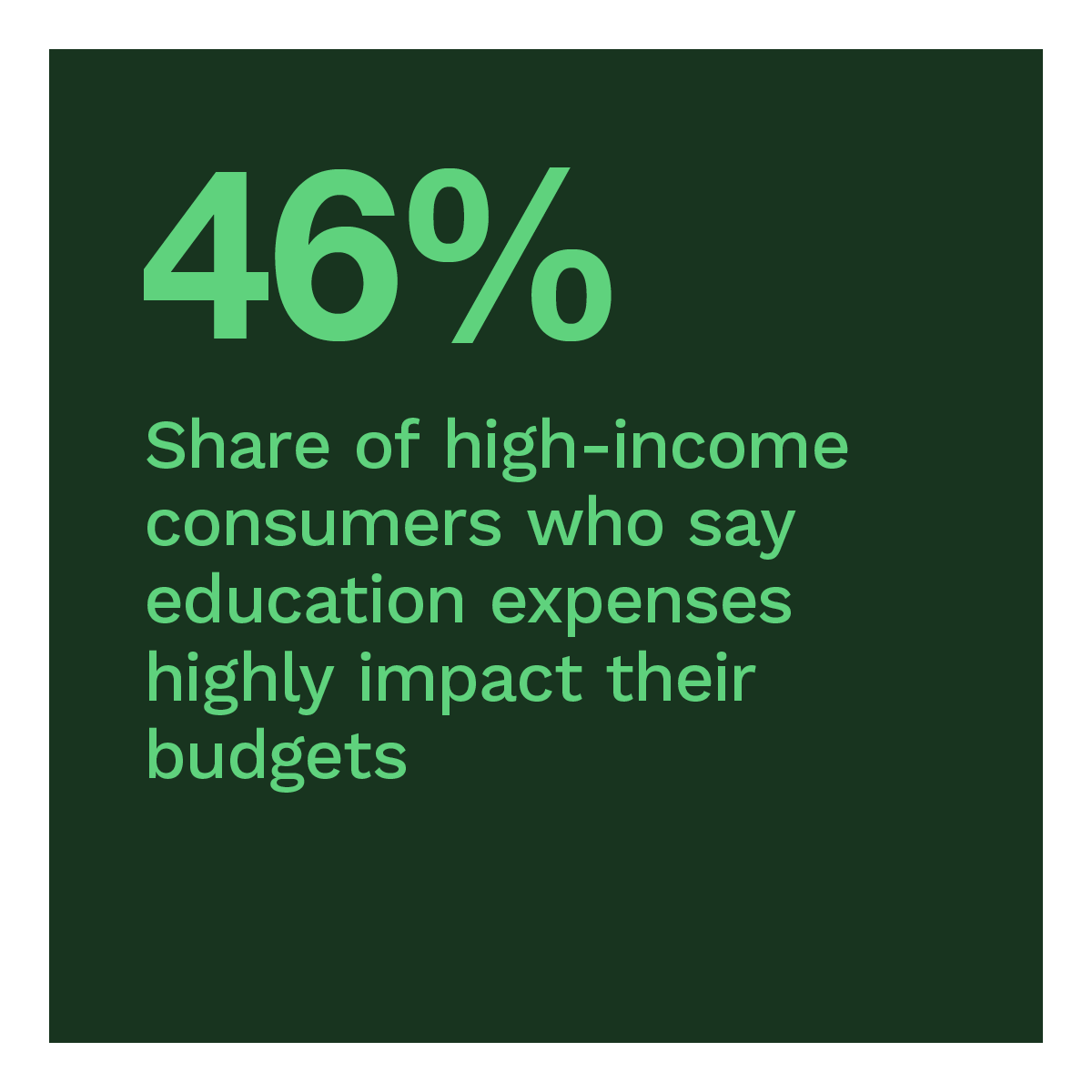

Even as housing and food costs rise, more affluent consumers report that essential spending represents a smaller fraction of their budgets than lower-income consumers. Discretionary spending on leisure, personal care and everyday transactions represents close to one-third of higher-income consumers’ available income. Higher incomes may also encourage consumers to engage in newer types of fixed expenses. For instance, those at the upper end of the income distribution are 54% more likely to be paying for education.

As income grows, the likelihood of saving usually increases. However, many high-income earners do not set aside fixed portions of their incomes. In fact, close to 1 in 5 consumers annually earning more than $100,000 have not saved every month in the last quarter. Adding to that, just 1 in 10 say they are non-savers. High-income earners are the likeliest to say they lack good saving habits. One possible explanation is that they may have less incentive to save than the average consumer as they are more confident about their job prospects and are less likely to switch jobs.

As inflationary pressures have subsided from their July 2022 peak, high-income consumers have rapidly increased discretionary spending. However, even they could benefit from finding ways to budget for essential and nonessential items to better live within their means. Download the report to learn about the financial stressors and spending habits causing high-income consumers to live paycheck to paycheck.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More