Almost 57 years ago to the day, the 1960’s rock band The Byrds appeared on the Ed Sullivan Show to sing their number one hit “Turn, Turn, Turn.” A song originally written by Pete Seeger in the 1950’s, it’s said to be one of the few songs based on Biblical verses to rise to the top of the Billboard charts. The lyrics, adapted from Ecclesiastes 3:1-8, suggest that the natural order of life includes a time and place for everything — including a time to die.

Reading much of the mainstream press lately, one comes away thinking that the time and the place for the card networks, eCommerce and Alexa is more yesterday than tomorrow.

The card networks, the Financial Times reports, are destined to suffer the same fate as the Kodak camera at the hands of Elon Musk, crypto, Alipay, and Apple, among others.

The requiem has all but been written for the “colossal failure” that is Alexa, Amazon’s expensive and unprofitable distraction.

And we might as well just stick a fork in eCommerce, since COVID artificially inflated its relevance; consumers now shop like it’s 2019, ditching online in droves as they return to the physical store.

In some sense, none of these prognostications are new.

Analysts and pundits have been predicting the end of the card networks for decades, egged on by a series of new payments schemes over that time with “merchant-friendly” business models. The media panned Alexa from the beginning as a personal assistant in need of “smarts.” And the digital transformation of retail was its future for most of 2020 and 2021, until eCommerce’s triple-digit growth fell back to double digits and analysts said, “never mind.”

So, maybe there is a time and a place for everything. Like a time for using data and frameworks to understand the dynamics of platforms and how they ignite and scale before we declare them dead or dying.

The King is Dead, Long Live the King!

The general-purpose credit card will turn sixty-seven next year. The path to ignition over almost seven decades was wrought with the challenges facing any network trying to get off the ground: getting a critical mass of merchants and consumers on board, further complicated by creating a business model with the incentives for banks to issue those cards to consumers. Then, add the not-so-insignificant development of the technology necessary to clear and settle transactions between merchants and those issuing banks to provide liquidity for all parties.

| There’s a time for using data

and frameworks to understand the dynamics of platforms and how they ignite and scale before we declare them dead or dying. |

Not surprisingly, banks struggled to make profits in the beginning as cards were issued with little more than a rudimentary credit check to get accounts and drive volume. Fraud ran rampant. Paper-based processes were no match for consumers who racked up balances and couldn’t repay, nor for bad actors who gamed the system without any intention to ever pay. Some banks got so frustrated that they considered pulling the plug.

Here’s a great read documenting the birth of the credit card industry that is a must-read for anyone in and around it.

Today, Mastercard and Visa combined have 6.7 billion cards in circulation, an increase of 6.3 percent year over year. 63 percent of U.S. adults used a debit or credit card at the physical or digital point of sale to pay the last time they purchased groceries.

In the U.S., among consumers who made an online purchase in the last 30 days, 52 percent paid with a stored debit card at least once and 45 percent used a stored credit card. In the ten other markets PYMNTS has studied since January 2022, 43 percent of consumers used a network-branded card (debit or credit) to make their last purchase in store and 37 percent did so online.

The reason for branded cards’ consumer popularity can be summed up in two words word: certainty and trust. Consumers can stick a debit or credit card in their pocket and go just about anywhere in the world and make a purchase. Digital card issuance makes that possible for any number of general-purpose mobile wallets, too.

Consumers know what to do if the item they purchased needs to be returned. If their card is lost or stolen, consumers know that their issuing bank has their back. For the approximately half who are credit card revolvers, the ability to use one card to pay at any store and then manage their cash by repaying over time is the appeal. For consumers who don’t revolve, getting 20 or 30 days of float before settling the bill makes using them easy and convenient. Contactless cards make the process at checkout faster and easier than ever, something that became particularly convenient during COVID. Both Visa and Mastercard report the massive shift to contactless at the point of sale over the last 24 months.

Getting to Ignition

After their launch around 1966, it would take about two decades for credit cards in the U.S. to ignite and begin to scale, a tipping point buffeted by a long period of economic stability in the U.S. in the 1980s. It would take about 15 years for debit cards to get real traction.

Throughout, Visa and Mastercard continually invested to improve the speed and security of their rails to clear and settle volumes at scale globally and harden their systems against the growing cyber threat. Their global rails have become the foundation upon which FinTechs have built their own businesses, leveraging the ninety-two million global endpoints that they provide and the clearing and settlement capabilities they enable.

That’s not to say that something new couldn’t or won’t emerge to chip away at the share that they have globally. It’s also not a news flash to Mastercard and Visa that challengers are circling the waters.

The card networks’ investments in a variety of initiatives — installments, push to card/instant payments for P2P, retail and commercial use, tokenization, network-of-networks/network-as-a-service model to enable any form of payment between consumers and businesses across their rails, cross-border and domestic payments initiatives, and virtual card programs for retail and commercial use cases — acknowledge the threats to their core business.

These investments acknowledge the traction that once-nascent payment alternatives like Buy Now, Pay Later, Open Banking and Real Time/Account-to-Account Payments are getting in many global markets — and the potential challenge they could pose in the future. Not to mention the divided loyalties of banks who see the opportunity to leverage their lending, compliance, and treasury services capabilities to reach new customers and power new business models.

| It’s not a news flash

to Mastercard and Visa that challengers are circling the waters. |

In the B2B payments space where so much friction remains, the card networks acknowledge both the opportunity and the challenges they face to be competitive — and the products, business models and partnerships necessary to be at the decision-makers’ table.

But any successor must overcome the classic chicken-and-egg problem, complicated in payments by the massive requirement to process trillions of dollars of payments volume every year securely, reliably and in compliance with global regulators.

That’s what wannabees must convince stakeholders — issuers, merchants, and consumers — they will do, so that stakeholders have incentives to switch to something new: a trusted network with a business model that can help them drive their profits at scale and preserve payments choice for consumers and businesses.

Don’t Sweat the Irrelevant Stuff

That’s why no one should be at all worried about Elon Musk and Twitter’s Everything App.

Consumers may want the simplicity of a single app for their banking and payments transacting — and Musk may have payments chops and ambitions to create the “X” app — but the basis for payments and commerce is trust. When 91 percent of Twitter users say that some of what they see on Twitter is inaccurate or misleading, Twitter has a hard time checking that box for payments transactions. Just because the Chinese Super Apps got their start in messaging doesn’t mean that Twitter is destined for the same success because Elon Musk says so. And right now, Twitter is not much of an Anything-Besides-Tweeting app.

I also wouldn’t be too concerned about Apple on a global scale. If anything, Apple Pay demonstrates the complexity of getting a new payments network off the ground and the challenge of convincing people to use a new way to pay that doesn’t offer a new source of value. After eight years, Apple Pay in the U.S. remains at 4.1 percent of retail transactions, according to the latest PYMNTS research, and even less on a global scale, excluding the U.K.

Everywhere, Apple Pay’s toughest competitors are the card networks, PayPal and — outside of the U.S. — local mobile schemes. Even if Apple Pay were to suddenly gain a head of steam, it maxes out at 50 percent of the U.S. market, and even less everywhere else, given the popularity of Android phones outside of the U.S.

Right now, Apple Pay depends heavily on the card networks and card issuers for payments. For Apple Pay — or any Big Tech player — to fully challenge them, they would have to convince users to switch from using their registered card credentials to their bank accounts for debit purchases and create installment payments options for any purchases they wish to make using credit. Not impossible, but far from a slam dunk.

Then there’s crypto. Is anyone really having this discussion now?

What will be interesting to watch is the emergence of new “on us” networks with direct consumer-merchant relationships. Two such networks exist today in the U.S. — Amex and Discover. PayPal with its 426 million active accounts (which may represent some users with multiple active accounts) is a hybrid whose success reflects the ability for consumers to use any method of payment, including network-branded cards, inside of its wallet.

Many posit that J.P. Morgan could become a successful card network challenger. The ten-year deal that J.P. Morgan signed with Visa in February 2013 gave it the ability to negotiate fees directly with merchants, which means it functions very much like a closed-loop network today with JPM card transactions processed over VisaNet rails. Then again, did I mention that was a ten-year deal?

More interesting, potentially, is how J.P. Morgan will use its investments, including those in hospitality/travel bookings services, to potentially challenge Amex and its Platinum cards for the very lucrative consumer and business travel segments.

| What will be interesting

to watch is the emergence of new “on us” networks with direct consumer- merchant relationships. |

Hey Alexa – How Does an Operating System Make Money?

Since its debut on November 6, 2014, consumers have connected more than 300 million devices to Alexa. Device manufacturers have used Alexa’s APIs and SDKs to voice-enable everything from appliances to thermostats, doorbells, garage doors, security cameras, blinds and lights.

That’s in addition to one hundred million smart speakers that Amazon has sold over the last eight years and consumers who use the Alexa app on their smartphones. Some automobile manufacturers talk about their new cars not by make and model but by the voice assistant that comes with the car — Alexa.

More recently, Alexa has integrated with Matter, the open-source standard that makes devices interoperable across voice platforms and will accelerate the reality of the connected home. Matter is the voice standard that 550 tech companies have already agreed to use; 280 device manufacturers have already signed on to have their devices compatible with it. In July, Amazon released its Ambient Home Smart Home SDK for developers to embed Alexa into any device, and October of 2022 saw the first release of devices using the Matter standard.

Only three hundred million devices are powered by Alexa? No wonder the media is trashing it.

The Alexa doom and gloom headlines followed a series of stories about Amazon’s cost-cutting efforts, which included slashing costs from its Worldwide Digital unit that includes Alexa. It’s that unit which is said to be on target to lose $10 billion dollars by the end of 2022. Worldwide Digital includes all hardware devices, including the Echo family of voice-activated devices, as well as Prime Video. Details related specifically to Alexa and its losses are scant.

Reports speculate that Alexa is unprofitable because the sale of speakers can’t cover its costs. And since consumers aren’t using Alexa enough to buy things, transaction revenues aren’t enough to close the revenue gap.

It’s easy to see how both of those things could be true. It’s also not how an operating system makes money or adds value to an ecosystem.

Embedded Alexa

Alexa is the third operating system of the digital economy — iOS, Android, and Amazon’s Alexa — something that I wrote in September of 2021 after reports were first released about Amazon’s slowing Echo speaker sales. Alexa is cross-platform, cross-device, and its user interface is as ubiquitous as it is easy to use: voice.

Early attempts to produce and integrate Alexa into Amazon-produced hardware were to get consumers comfortable using it, gathering intelligence about how it was used and where opportunities existed for further monetization.

The ambition, perhaps not publicly articulated as such, was to make Alexa the foundation for an ambient, always-on, voice-activated commerce ecosystem. Keep in mind that with every Alexa-enabled device, there is also an Amazon Pay credential connected to its vast commerce ecosystem.

That makes the Alexa operating system capable of making a sale and fulfilling an order without introducing any friction to the consumer or the merchant, and that capability comes embedded into the smart devices people have in their homes, and the many more they will acquire and use over time.

| Alexa’s business model is

just like any other operating system: License its use, share revenue from users’ sales and give advertisers a new channel to a captive audience. |

Today, PYMNTS research suggests that only 1.9 percent of consumers in six global markets use Alexa to purchase groceries and other retail items — piddly and not very much at all. Early adopters include Gen Z and Millennials, mostly for things that are not complicated to order, like groceries.

Alexa’s future, though, is one where she won’t wait for consumers to ask her to do things, but instead remind them to reorder items before they run out — all using intelligence based on order history and usage patterns.

Alexa will also likely use the real-time data from devices to troubleshoot maintenance problems by sending alerts and suggestions for repair or replacement. It could make those data available to third parties who want to know how to improve the quality of the products they produce. We’ve already seen how data from its Ring doorbells has been shared, with permission by the user, to make communities safer.

Alexa can, over time, also suggest makes and models and brands based on preferences as well as recommendations from other users.

That makes Alexa’s business model just like any other operating system: licensing its use to app developers and device manufacturers, sharing revenue from sales made to those that enable it and giving advertisers a new channel to introduce their brands to a captive, relevant audience.

Clearing the eCommerce Smoke and Mirrors

Wait, this can’t be right.

According to PYMNTS’ 2022 national Black Friday study of 2,439 consumers, more of them shopped online on Black Friday (25.8 percent) than in the physical store (17 percent). And the number of consumers who shopped in the physical store decreased 23 percent year over year.

I guess these consumers forgot that online shopping is off the table now since we’ve all gone back to the physical store.

Such is the claim of analysts and pundits who point to the consumer’s return to the brick-and-mortar store in 2022 as evidence of their waning appetite for digital shopping. More specifically, they say that the shift to digital during COVID was a temporary blip; now that COVID is in their rear view, consumers have all gone back to their 2019 habits. The permanent shift to digital because of the habits formed over the 2020/2021-time frame never happened.

That’s flat out wrong.

Naturally, the highest use of eCommerce channels happened in Q2 2020 — at 16 percent of sales — for the obvious reason. The levels have moved up and down since then, dropping to 14 percent by the first quarter of 2022 and more recently increasing to a seasonally-adjusted level of 15 percent in Q3 2022.

At the same time, consumers have gone back to the physical store, something that started to happen in 2021, and increased even more in 2022.

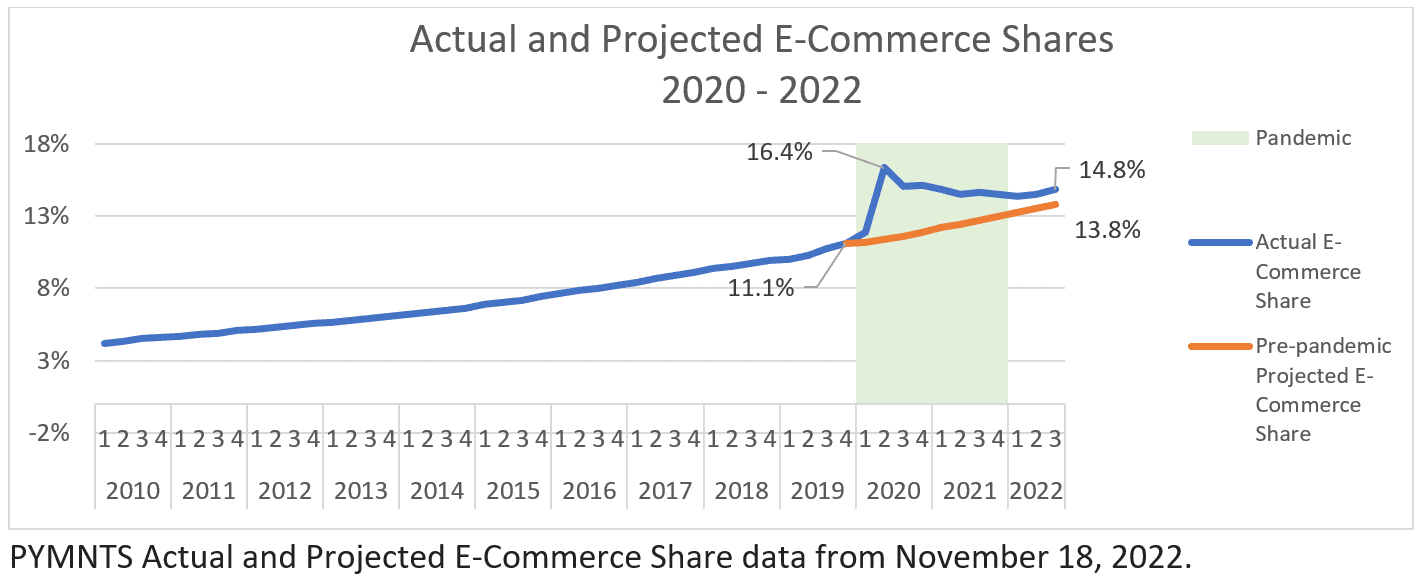

But look at this chart that compares U.S. Census data, and projections of eCommerce sales based on e-commerce share data from 2010 to Q4 2019 (the last quarter before the pandemic began) with ecommerce sales reported by Census.

What’s clear is that eCommerce did get a permanent bump because of the digital habits honed during COVID, and PYMNTS calculates that to be approximately one percentage point higher today than it would have been (13.8 percent) without the increase in use of digital channels by consumers between 2020 and 2022

Source: PYMNTS.com, U.S. Census Bureau Data. Estimated Quarterly U.S. Retail Sales (Seasonally Adjusted): Total and eCommerce.

So — big deal and so what, you might say — what’s one percent? That one percent represents an additional $81.6 billion in eCommerce sales over the last four quarters, or an 8% increase in eCommerce sales that can be solely attributed to the increased use of digital channels to make purchases between 2020 and 2022. According to Census data, total retail sales over the last four quarters were $7 trillion, and $1 trillion of these retail sales were made via eCommerce techniques.

This analysis is courtesy of PYMNTS analysts and tested across a variety of statistical models and estimation procedures. It also reflects the silent revision by Census of their eCommerce sales estimates over the course of the pandemic, which I summarized in a piece published in May of 2022.

Soon-to-be-released PYMNTS data for six large countries shows similar patterns: even as consumers went back to the stores more than they did in 2020 and 2021, they aren’t shopping in those stores as they did in 2019. Digital is down slightly, but way up over levels recorded pre-pandemic.

In fact, consumers now bucket their shopping into digital for the things they don’t need to see and inspect, which is a lot of retail and CPG products, and in-store for things they would like to inspect before buying — groceries, some electronics and home furnishings.

None of this should come as a surprise. Physical retail has been in a serious state of decline since 2010 with massive store closings each year — including 9100 alone in 2019. Consumers may be heading to stores more now than they were during the pandemic, but they are still using eCommerce more than they would have had the pandemic not occurred.

And that is a fact.

For more proof, check your front porch to see how many boxes from orders placed online are there.

| Digital is down slightly,

but way up over levels recorded pre-pandemic. |

Frameworks as Friend

Platforms power digital transformation across every facet of the global economy, many with stakeholders who compete one day and collaborate the next. Payments have helped monetize many of these new connected ecosystems and fuel the business models that provide new ways for consumers and businesses to engage.

The interdependencies of these platforms, new ecosystems really, make them challenging to understand. Frameworks can help.

Successful platforms must eliminate the frictions that exist today and improve the outcomes for the stakeholders who drive the financial success of the platform. Eliminating those frictions must save those stakeholders time, their most precious asset, and remove the uncertainty that keeps many interested parties from making a change. And do that at scale.

Like most successful platforms that have ignited, scaled, and operated successfully for many years, observers from afar believe creating a new one from scratch is easy-peasy.

Meanwhile, I can count on one hand, without using any of my fingers, the number of innovators who’ve started platform businesses and said it was easy.

I’ll need more than all my fingers and toes to count the ones that have crashed and burned.

With platforms, “turn, turn, turn” follows a different rhythm than life. New ones die quickly and only a few survive. Successful ones can be resilient and tough to displace, including those that have been around for some time and keep getting the job done.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More