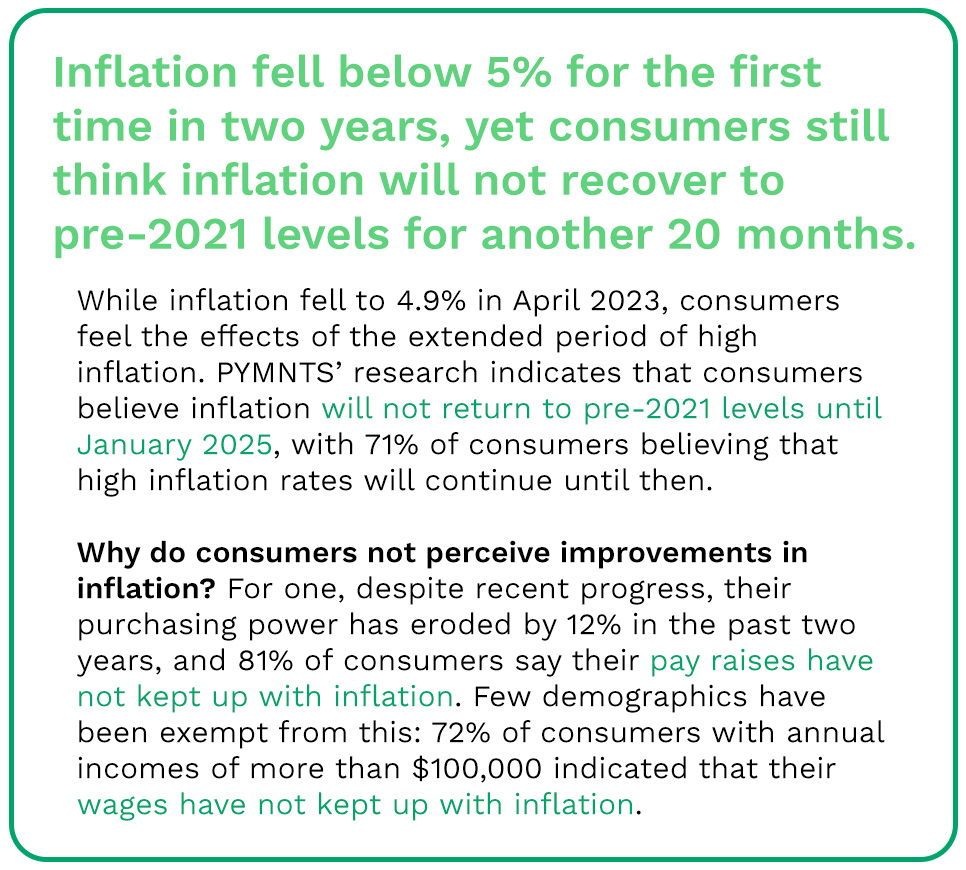

Inflation may be on a downward trajectory, but consumers do not think so, as perception affects their spending behaviors, prompting them to rethink how they use cash, debit and credit cards.

PYMNTS’ latest research sheds light on the impact of inflationary trends on United States consumer spending. The study finds that baby boomers and seniors and Generation Z prefer using cash more than other demographic segments.

This preference may partially be out of habit for baby boomers and seniors. Gen Z may not have as much access to cards as cash. Debit and credit cards remain U.S. consumers’ preferred replacement for cash, with debit assisting in the upswing in growth of digital wallets.

This report is the 11th installment of the “Consumer Inflation Sentiment Report” series exploring consumers’ outlook on the American economy. The “Consumers, Cash and the Inflationary Economy” edition examines the evolving role of cash and digital payments in consumer spending behaviors as inflation and political uncertainty continue to shift the economy. PYMNTS surveyed 2,138 U.S. consumers between May 4 and May 11 to better understand how inflation impacts their perceptions of spending and payment preferences.

This is what we learned.

Although 94% of consumers used cash in July 2018, the world has changed. The share of U.S. consumers carrying cash is declining — in August 2020, 84% of consumers used cash.

This share is down to 81% as of April 2023. Cash is being phased out even among those using it, as 33% of cash-using consumers say they carry less than before. Among all consumers, just 21% say they are keeping more cash on hand, although the extent to which they have increased this is driving up average figures.

Overall, 19% of consumers in the U.S. no longer regularly carry cash. Women, Generation X consumers and those with lower incomes are more likely not to carry cash than other demographics. Although 14% of consumers annually earning more than $100,000 report not using cash, nearly one-quarter of those earning less than $50,000 have moved on from using it.

Since January 2021, prices have increased by 17%, and the cost of retail products has increased by more than 22%. As alluded to before, cash users seem to have responded to these increased prices by increasing the amount they carry, averaging $79 today compared to an average of $63 in August 2020.

So, who is using cash? Interestingly, Gen Z and baby boomers and seniors are the most likely to carry cash, at 85% and 84%, respectively. But the similarities between these two demographics seems to end there. Gen Z carries the most cash across all demographics, at $116. Baby boomers and seniors carry nearly half as much, at $63. These numbers may trend closer to each other in time, as 35% of Gen Z consumers say they now use less cash than they did one year ago, leading all generations.

Our data shows that cash still has some versatility in consumers’ minds, and motivations to hang on to it vary.

For consumers, some purchases still seem too small for cards. Forty-five percent carry cash for small purchases such as a cup of coffee, snacks from vending machines, fresh produce from farmers’ markets or on-the-spot donations. Gen Z tends to use cash more than other demographics, suggesting they are less likely to own debit or credit cards.

Next is inertia. PYMNTS found that 40% of U.S. consumers today carry cash out of habit, especially baby boomers and seniors. Twenty percent of all consumers identified this as the most important reason they carry cash, narrowly edging out the 19% who identified small purchases as the top reason.

An enduring use case for carrying cash and making cash payments — regardless of gender, generation or income level — is tipping. Tipping played a uniquely supportive role during the pandemic’s peak when consumers with disposable income increased the amount they tipped to support local businesses and restaurants. Today, 46% of consumers say they have used cash to leave a tip at a restaurant or small business in the last 30 days.

Fifty-one percent of consumers who currently carry cash but have used it less in the last year say that the ease and convenience offered by other payment methods prompted this change in their behavior. The eroding buying power of consumers has increased the pressure they feel to pace their spending and budget more carefully. In April 2023, it would take $100 to buy what $88.20 could have bought in April 2021.

Twenty-five percent of consumers today carry less cash than last year, as they now find carrying the amount needed for daily use impractical. Sixteen percent of baby boomers and seniors and 14% of Gen X consumers felt most bothered by the prospect of carrying more cash.

The reduction in access points for cash — namely bank branches and ATMs — is another factor making cash less desirable. Twenty-three percent of consumers say they use less cash because accessing it is too difficult, further increasing the appeal of other payment methods.

PYMNTS found that for consumers who do not carry cash, 81% replaced it with debit cards and 58% with credit cards, confirming the enduring popularity of cards in consumer spending.

Digital wallet options such as PayPal, Apple Pay and Cash App are building on the infrastructure provided by cards while enabling peer-to-peer transactions. While digital wallet use paints a picture of where payments may head, consumers reducing or discontinuing their use of cash prefer debit and credit cards to other digital payments.

Although cash had already begun to lose popularity among consumers in the U.S., inflation has further discouraged them from carrying the large amounts required to make daily purchases. This has made alternative payment methods — particularly debit cards — more attractive. Today, 19% of Americans no longer carry any cash, an increase of 3 percentage points since 2020.

While cash maintains a role in daily life, debit and credit cards are increasingly popular alternatives. This shift is good news for those relying on interchange revenues, such as card networks, payment processors and card issuers. Just as one of cash use’s strongest pulls is the habit of using it, the steady presence of cards in the economy for nearly half a century has pushed greater adoption of them than that of digital wallets. In the long term, digital wallets stand to gain ground due to their connection to the foundation that cards have laid in making cashless transactions common.

“Consumer Inflation Sentiment Report: Consumers, Cash and the Inflationary Economy,” produced independently by PYMNTS, examines and analyzes inflation’s impact on consumers, the types of payments they prefer and the reasons behind those preferences. We surveyed 2,138 U.S. consumers between May 4 and May 11 about their experiences and perceptions. The sample was balanced to match the U.S. adult population in key demographic variables. Our respondents’ average age was 48, 51% were female and 37% annually earned more than $100,000.

Read the May “Consumer Inflation Sentiment Report: Consumers Cut Back by Trading Down” and other previous editions of the series for more.