Nearly half of financial institution executives are concerned that open banking may not be a positive value proposition — especially in an environment of increasing fraud.

Forty-six percent of FIs said the potential for accelerated fraud outweighs any rewards they see in open banking, according to the PYMNTS Intelligence study “How Fraud Fears Impact FIs’ Adoption of Faster Payment Solutions.” For FIs that are already experiencing higher levels of fraud, the percentage of open banking skeptics jumps to 57%.

These are key findings from the report, based on a 2023 survey of executives representing 200 FIs in the United States who were asked to share their thoughts on open banking, fraud and instant payments.

Open banking is a legal framework permitting third-party FinTechs to access FI financial data to fuel the products and services they offer customers. In October, the Consumer Finance Protection Bureau (CFPB) urged the financial services industry to “accelerate” its shift toward open banking.

CFPB Director Rohit Chopra said in a statement that he believes open banking will “supercharge competition, improve financial products and services, and discourage junk fees” — all while empowering consumers to “walk away from bad service and choose the financial institutions that offer the best products and prices.”

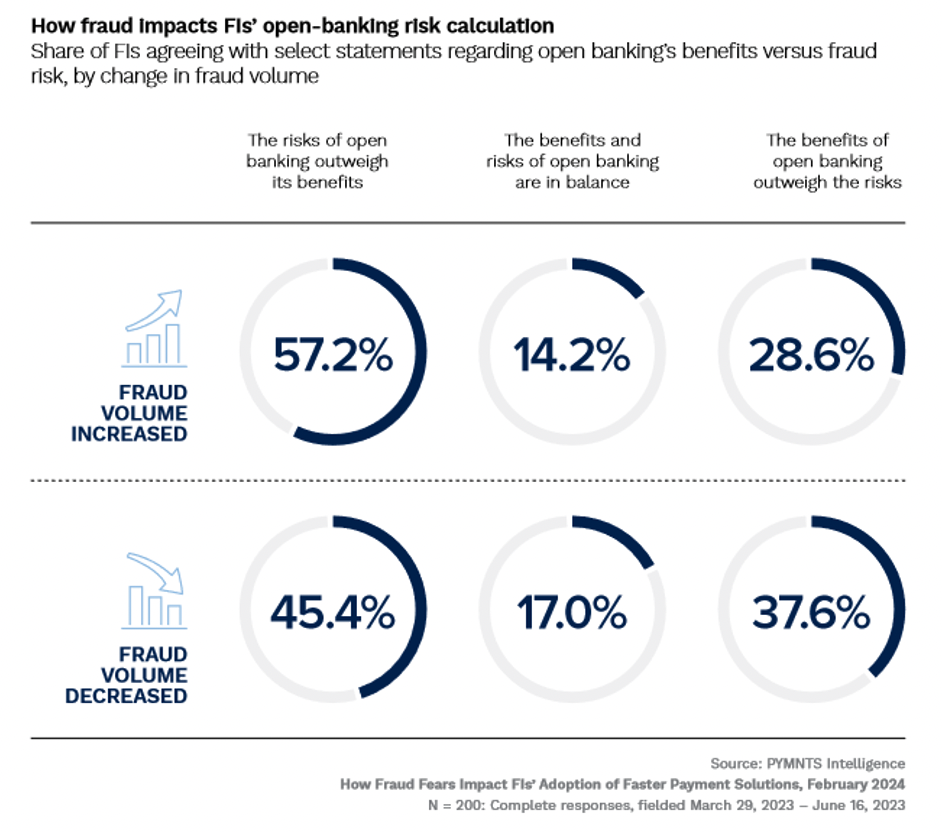

However, the PYMNTS Intelligence study revealed that FIs are less enthusiastic, with many fearing that open banking will supercharge fraud. Only 35% of the FIs surveyed believe the perks will outweigh the risks.

The report showed in most cases, smaller FIs expressed enthusiasm, perhaps because they believed open banking might provide them with a competitive edge.

Meanwhile, more than half of the largest FIs — those with more than $100 billion assets under management — said the risks dwarf the rewards primarily because of the potential for increased fraud.

Institutions now experiencing high fraud volumes told PYMNTS Intelligence they’re concerned that the proposed framework could lead to even higher fraud volumes. Conversely, nearly 38% of FIs with lower fraudulent transaction volumes said open banking’s upside outweighs any downside.

Increased payment speed is another decisive factor in the open banking debate.

Most FIs — 52% — said consumer demand for increased payment speeds brings with it new fraud vulnerabilities, and they fear open banking will only intensify that risk. Although another 28% shared the belief that faster payments mean more risk, they said the various benefits negate the risks.

Things change slightly when the conversation turns to real-time payments. The survey found that 81% of all respondents were confident in their ability to provide secure real-time payments — a feature open banking should accelerate.

But, unlike the other trends identified in the report, the confidence FIs expressed in their ability to facilitate secure real-time payments dropped slightly with institution size. Nearly all FIs with $100 billion assets under management said offering real-time payments would not compromise their security; however, only 78% of FIs with assets under management between $1 billion and $5 billion voiced similar confidence.

Likewise, those FIs that were already using cloud-based security systems as well as artificial intelligence and machine learning solutions were more confident in their ability to fully manage risk in an open banking environment. This suggests that onboarding advanced fraud prevention technologies now may help even skeptical FIs transition to the inevitable open banking landscape.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More