Consumers are drifting deeper into financial uncertainty while scrambling to cover costs.

There seemed to be little cause for concern about consumers’ ability to spend and save after having built up reserves during the pandemic, as Fed-released numbers in October revealed that U.S. households held $1.7 trillion in “excess” personal savings. Any relief dissipated, however, when details revealed that distribution to be disproportionate, with households in the top half of income distribution holding 75% of those funds.

Indeed, these concerns were borne out, as 12% of consumers spent more than they earned in the six months preceding October. To cover these expenses, 27% of households pulled from savings to manage credit card debt alone, and 35% of that “extra” pandemic-era savings had evaporated by February. Additionally, a record number of 401(k) plan holders dipped into their plans to cover costs in 2022.

More recently, savings don’t even cover credit card debts for many paycheck-to-paycheck consumers, as those with issues paying their bills carry average balances comprising 157% of their available savings.

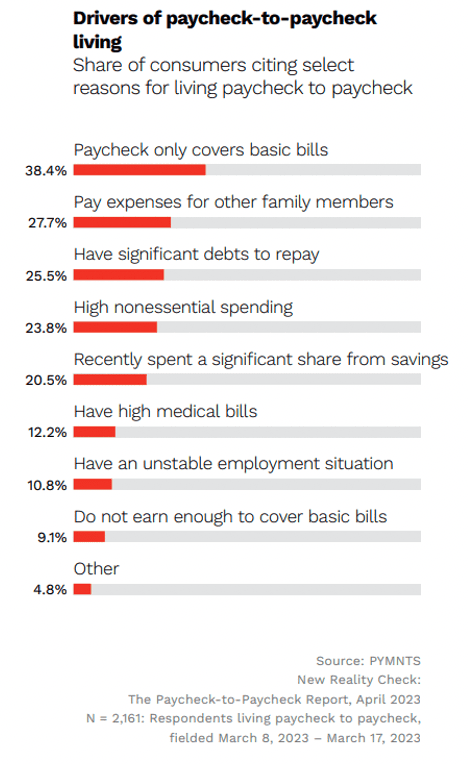

And now, as noted in PYMNTS’ latest collaboration with LendingClub, “New Reality Check: The Paycheck-to-Paycheck Report,” dipping into savings significantly is a driver behind nearly 21% of consumers living paycheck to paycheck.

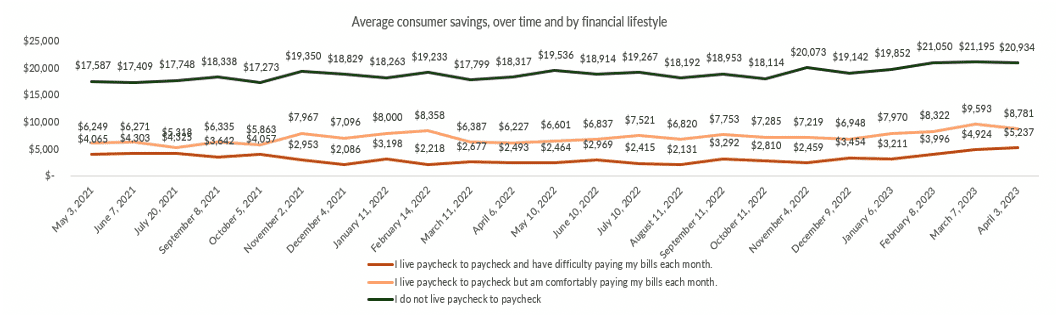

Good news for some, at least, comes when breaking the data down further by time and financial lifestyle.

Consumers living paycheck to paycheck with no bill pay issues and those not living paycheck to paycheck saw their average savings climb at the start of the year and slightly decrease at the start of April. One may assume this decrease is due to further using savings to cover expenses, although a more formed picture may become apparent in the coming months.

However, the opposite has been true during the same period for those living paycheck to paycheck with bill pay issues. This may be due to a tighter labor market in recent months, which has led to wage increases in certain sectors. However, it should be noted that the savings rate among this financial lifestyle may change, as variables such as recently decreased SNAP benefits could affect those with bill pay issues’ saving ability.

Dipping into dwindling savings is driving some consumers into living paycheck to paycheck. As inflation fears evolve into recession chatter, that number may rise in the coming months, leaving many more consumers open to scraping their savings to cover everyday costs.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More