As the financial landscape continues to evolve, traditional banks face an increasing challenge from digital-native FinTechs. The recent surge in buy now, pay later (BNPL) services presents both a threat and an opportunity for banks striving to regain a foothold in a market shifting toward digital convenience.

A PYMNTS Intelligence report, “Build Now, Not Later: How Banks Can Seize the BNPL Opportunity,” created in collaboration with Galileo, examines crucial insights about the current BNPL trend and its implications for traditional financial institutions (FIs). Here are three takeaways from the report that illustrate the importance of BNPL services in shaping the future of banking.

The popularity of BNPL services has seen remarkable growth, driven primarily by younger, digitally savvy consumers. This trend is particularly evident during peak shopping seasons; for instance, consumer spending on BNPL transactions reached $17 billion between November and December, marking a 14% increase from the previous year. This surge indicates a clear shift in consumer preference toward flexible payment options that allow for the deferral of costs without incurring significant interest.

The appeal of BNPL services lies in their seamless, user-friendly nature. Customers appreciate the convenience of managing payments in small, manageable installments, which helps alleviate financial strain during uncertain economic times. Despite this popularity, there are areas for improvement; a portion of BNPL users desire lower fees and enhanced application processes. This presents an opportunity for both FinTechs and traditional banks to refine their offerings and capture a larger market share.

In response to the growing consumer demand for BNPL options, many banks and financial institutions are beginning to roll out their own BNPL services. This shift is a strategic move to attract and retain customers who might otherwise turn to FinTech competitors. For example, U.S. Bank has launched its own BNPL service, Avvance, which offers financing and repayment plans at the point of sale and is designed to integrate with existing merchant relationships.

Additionally, partnerships between banks and third-party providers, such as the collaboration between Marqeta and Credi2, are helping financial institutions to expedite their entry into the BNPL market. These alliances allow banks to offer BNPL solutions quickly and efficiently, leveraging the technological capabilities of their partners while tapping into the existing customer base of the banks.

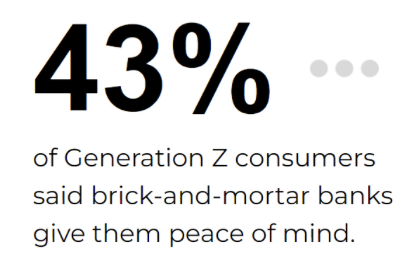

Although FinTech companies initially pioneered the BNPL space, traditional banks are rapidly catching up. Banks possess inherent advantages that could position them favorably in the BNPL market. A key factor is consumer trust; surveys indicate that a notable portion of Generation Z consumers and other demographic groups have greater confidence in banks compared to FinTechs, particularly concerning fraud prevention and overall financial security.

Although FinTech companies initially pioneered the BNPL space, traditional banks are rapidly catching up. Banks possess inherent advantages that could position them favorably in the BNPL market. A key factor is consumer trust; surveys indicate that a notable portion of Generation Z consumers and other demographic groups have greater confidence in banks compared to FinTechs, particularly concerning fraud prevention and overall financial security.

Banks possess established infrastructures, extensive customer data and advanced risk assessment capabilities. These resources enable them to develop customized BNPL solutions with strong fraud protection and credit management features. By utilizing their experience and existing customer relationships, banks are positioned to offer BNPL services that are secure and seamlessly integrated into their overall financial offerings.

The rise of BNPL services marks a transition toward flexible financial solutions. Banks are entering this market, using their infrastructure and customer base to provide secure, integrated BNPL options. This move offers banks a chance to capture market share and influence the future of financial services by meeting demands for convenience and affordability.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More